Be On the Safe Side by Having a View of Your Tax Withholding Today!

If you’re an American receiving a pension, then looks like you could be in for a scary surprise this coming year.

That’s because judging from the previous year’s tax overhaul, it appears that quite a number or pension payments have increased, resulting in the lower tax rates that have been put in place since 2018.

Pension payments withholding

However, this new bump is expected to increase the risk of recipients having their pensions underwithheld come the next tax time the following year. Thus being subjected to a penalty. To avert such a situation, retirees will then have to immediately have a look at their withholding and proceed to have it adjusted if deemed necessary.

One pensioner who will be confirming hers is Ann Gardella. Being a music teacher retiree, she now lives in Southbury, Conn. For her, a majority of her income is derived from her pension, which is now proving a financial hurdle because monthly payments have risen. Moreover, the fact that she has a tax balance to look forward to every April, calls for the fact that she has to go over her withholding.

She says that she plans not to owe any penalties the following year.

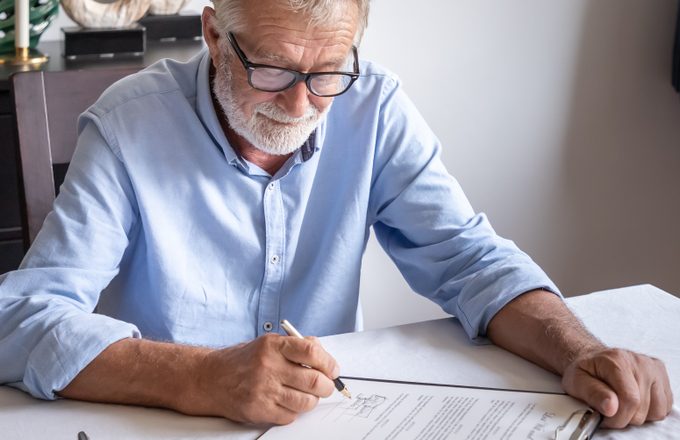

Milos Vucicevic/Shutterstock

The sudden increase in pension payments is proving financially straining for some retirees, with some opting to have their withholding looked at to avert the situation

A thorn in the side

The current predicament of pensions is somewhat identical to the current paycheck affair. As a matter of fact, earlier in 2018, Treasury officials proceeded to modify withholding tables in a bid for them to replicate changes this 2018 that were as a result of the previous year’s tax overhaul. Now, these said changes have been added to employee paychecks as well as pension payments.

However, these adjustments did not consider the overhaul changes. For instance, the withholding tables that are currently in place have an additional tax-rate change, however, the $10,000 cap has not been factored in for both local and state taxes.

Therefore, the upside is that a number of pension recipients could inevitably end up being underwithheld this 2018 due to their automatic adjustments being directed to their pension payments being too high to handle.

Avoiding tax penalties

Generally, people have to pay at least 90% of owed tax within a year; or alternatively, the next mid-January if they have been making their tax payments with a quarterly plan. The current penalty is a 5% annual interest.

That being said, pension payments tend to vary widely, so it could be quite difficult to predict individuals at the highest risk. However, for the average married individual has a $50,000 pension a year, the reduction with regard to withholding amounts to roughly about $818 a year. This cuts down withholding to about 20%. Hence, a pension payer who opts to follow the government’s table structure is not liable if the recipient becomes underwithheld.

Casper1774 Studio/Shutterstock

The new and more stringent methods have been put in place, meaning that retirees have to be more involved in terms of their pension payments.

This new facet in the realm of pension payments has become another motive for why retirees- specifically those that have gone into retirement recently or have been working part-time- should be on the lookout for any ‘tax shocks’ that may come their way.

That being said, for quite a number of retirees, income just doesn’t plummet. If anything, it is usually lumpy, specifically if someone is doing some side work. Moreover, medical expenses may be rendered deductible for first timers, with additional deductions being introduced when the individual reaches the age of 65.

More in Mind & Mental

-

`

Signs of Emotional Connection in Relationships

Signs of Emotional Connection in RelationshipsBuilding a strong connection with someone isn’t just about being in sync or sharing hobbies—it’s about that deeper bond, where you...

December 4, 2023 -

`

Hollywood’s Shortest Marriages: Britney Spears, Carmen Electra & More!

Hollywood’s Shortest Marriages: Britney Spears, Carmen Electra & More!In the glitzy world of Hollywood, where fairy tales often unfold on the silver screen, there exists a flip side—a realm...

December 3, 2023 -

`

The Surprising Benefits of Unplugging

The Surprising Benefits of UnpluggingIn today’s hyper-connected world, where we are constantly bombarded with notifications, messages, and the allure of social media, disconnecting may seem...

November 26, 2023 -

`

How “Looking Your Best” Improves Our Wellbeing

How “Looking Your Best” Improves Our WellbeingMost of us have had moments standing in front of our closet, deciding on an outfit for the day. And we...

November 15, 2023 -

`

Therapy? Medication? What Are the Treatments for PTSD

Therapy? Medication? What Are the Treatments for PTSDPost-Traumatic Stress Disorder (PTSD) is a common after-effect of traumatic events. It can be a debilitating condition, but the good news...

November 7, 2023 -

`

Meet the Woman Who ALMOST Married Barack Obama

Meet the Woman Who ALMOST Married Barack ObamaBarack Obama’s life has been a captivating narrative, often told and retold, with each revelation adding layers of intrigue to his...

November 5, 2023 -

`

The Rise of Caviar Bumps, Thanks to Gen Z

The Rise of Caviar Bumps, Thanks to Gen ZIn an intriguing twist of culinary culture, millennials and Gen Zers are drawn to an unusual indulgence – fish eggs, or...

October 28, 2023 -

`

Everything You Need to Know About Acid Reflux, Heartburn and GERD

Everything You Need to Know About Acid Reflux, Heartburn and GERDEver had that burning-in-the-chest sensation after a meal? Or perhaps you have lain awake at night with an odd sour taste...

October 17, 2023 -

`

Best AI Apps for Mental Health

Best AI Apps for Mental HealthMental health has long been a topic of discussion and concern. With technological advancements, AI (Artificial Intelligence) has emerged as a...

October 10, 2023

More From PsychicMonday

-

Essential Mexico Travel Tips for a Seamless Adventure

Essential Mexico Travel Tips for a Seamless AdventureMexico, a land of vibrant culture, breathtaking landscapes, and mouthwatering cuisine, beckons travelers from across the globe. But before you embark...

LeisureApril 16, 2024 -

9 Common Dreams and Their Messages in Your Dreams

9 Common Dreams and Their Messages in Your DreamsHave you ever woken up in a cold sweat, heart pounding, after a particularly vivid chase sequence in your dreams? You’re...

Mind & MentalApril 9, 2024 -

How to Let Go of the Past – Practical Strategies for Moving On

How to Let Go of the Past – Practical Strategies for Moving OnWe’ve all been there. A broken heart, a shattered dream, a painful betrayal – these experiences leave their mark, etching themselves...

SpiritualApril 1, 2024 -

Understanding Emotional Cheating – How to Identify, Address, and Recover

Understanding Emotional Cheating – How to Identify, Address, and RecoverEmotional cheating, often an unspoken specter in relationships, can silently erode trust and connection. It’s the subtle betrayal of emotional intimacy,...

Love LifeMarch 26, 2024 -

Letting Go and Living Lighter: Your Guide to Stress Release

Letting Go and Living Lighter: Your Guide to Stress ReleaseStress. It’s a constant companion in our modern world, showing up in the form of work deadlines, traffic jams, relationship woes,...

Mind & MentalMarch 18, 2024

You must be logged in to post a comment Login